Time Limit for Issuing GST Notice Under Section 73 & 74: A Complete Guide for 2025

Time Limit for Issuing GST Notice Under Section 73 & 74: A Complete Guide for 2025.

Rhushikesh C Patil

12/18/20254 min read

Time Limit for Issuing GST Notice Under Section 73 & 74: A Complete Guide for 2025.

If you are a business owner or a taxpayer, you might worry about the tax department suddenly asking for records from years ago. Can they send a notice whenever they want? The short answer is no.

The GST law has specific "expiry dates" (called limitation periods) for sending notices and passing orders. Most common notices fall under Section 73 of the CGST Act. Let’s break this down into simple terms.

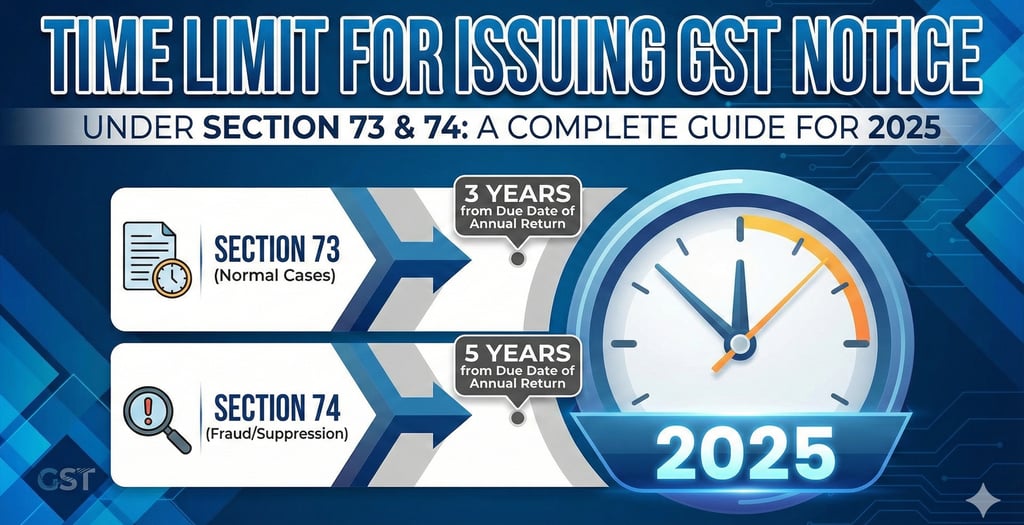

What is Section 73?

Section 73 applies when you have underpaid tax, claimed too much Input Tax Credit (ITC), or received an incorrect refund by mistake. This is for cases where there is no fraud or intention to cheat the government. It’s for honest errors, like a calculation mistake or a misunderstanding of a rule.

The 3-Year Rule

The law says the GST officer must finish the case (pass the final Order) within 3 years from the deadline for filing the Annual Return for that year. To give you time to defend yourself, they must send you the Show Cause Notice (SCN) at least 3 months before that 3-year deadline ends.

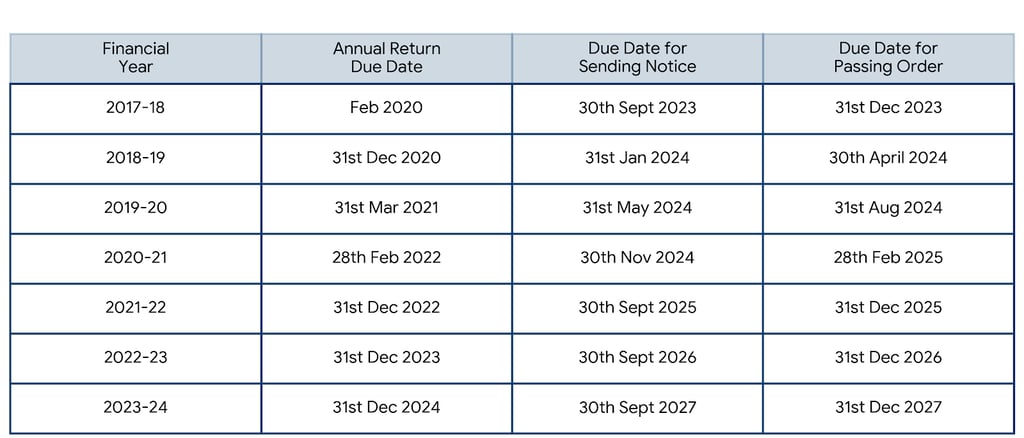

Important Deadlines to Remember

Because of the COVID-19 pandemic and initial GST hurdles, the government extended these dates. Here is a simple table to help you check if a notice you received is valid or "time-barred":

Quick Tip: If you receive a notice for FY 2017-18 or 2018-19 today, it is likely invalid because the legal deadline has already passed!

What if there is Fraud? (Section 74)

If the department believes you intentionally hid facts or committed fraud to avoid tax, they use Section 74. Under this section, they get more time because the offense is serious. They have 5 years (instead of 3) from the Annual Return date to pass an order. This means they can send a notice as late as 6 months before that 5-year window closes

Why Does This Matter?

If an officer sends a notice after these dates, the notice is legally "time-barred." You can challenge it solely on the grounds of delay, even if the tax calculation itself is correct.

The "New Regime" – A Paradigm Shift (From FY 2024-25 Onwards)

The Finance Act, 2024, brought about a massive structural change to simplify the limitation periods for future cases. It introduced a new Section 74A.

For any tax demands pertaining to the financial year 2024-25 and subsequent years:

The distinction in time limits between Fraud (Sec 74) and Non-Fraud (Sec 73) cases has been ELIMINATED.

The New Unified Timeline (Section 74A):

Under Section 74A, regardless of whether the case involves fraud or mere error, the time limit is unified:

Time Limit for Passing Order: The order must be passed within 42 months (3.5 years) from the due date of furnishing the annual return for the relevant financial year.

Time Limit for Issuing Notice: The notice under Section 74A must be issued at least 3 months prior to the date of issuance of the order. (Effectively, 39 months from the annual return due date).

Why is this important for 2025? While we won't see notices for FY 24-25 immediately, tax professionals must be aware that the strategy of differentiating between "suppression" and "error" to argue limitation periods will no longer apply for future periods. The Department now has a standard 3.5-year window for all cases.

Conclusion: Actionable Insights for Tax Professionals

As we move through 2025, your approach to handling GST notices must be bifurcated based on the financial year involved.

Key Takeaway for Drafting Replies:

When you receive a DRC-01, immediately check the Financial Year in question.

If it's for FY 2019-20 or earlier (under Sec 73): Check if the notice was issued before the extended deadlines listed in the table above. If not, challenge it immediately on the grounds of limitation.

If it's for FY 2024-25 (in the future): Remember that the "intention to evade" argument will no longer save the taxpayer from the extended limitation period, as the timelines have merged under Sec 74A.

Navigating these timelines requires precision. If you have received a notice and are unsure about its validity regarding the limitation period, always seek professional advice before filing your reply on the portal.

Frequently Asked Questions (FAQs)

1. Can the department send one single notice for multiple financial years?

Ans - Technically, they can issue a "statement" for multiple years, but courts (like the Madras High Court) have ruled that "bunching" multiple years into one notice is often invalid if it tries to bypass the individual limitation periods of each year. Each year has its own "clock."

2. What happens if I receive a notice even one day after the deadline?

Ans - If a notice is issued after the due date mentioned in the law (e.g., Nov 30, 2024, for FY 20-21), it is considered "time-barred." Recent High Court rulings have confirmed that these timelines are mandatory and the department cannot ignore them.

3. Does the deadline change if I haven't filed my Annual Return?

Ans - No. The limitation period is calculated from the actual due date of the Annual Return, regardless of whether you filed it on time or not.

4. Is there a different time limit for GST refunds?

Ans - Yes. For erroneous refunds, the 3-year (Section 73) or 5-year (Section 74) clock starts from the date of the refund order, not the annual return date.

5. What is the new Section 74A I’m hearing about?

Ans - Starting from FY 2024-25 onwards, the government has introduced Section 74A. This merges the deadlines for both fraud and non-fraud cases into a single 42-month window to issue a notice, simplifying the process for the future.

6. Can I still be penalized if I pay the tax before the notice is issued?

Ans - Under Section 73 (non-fraud), if you pay the tax + interest before the notice is issued, no penalty is applicable. Under Section 74 (fraud), you would still have to pay a 15% penalty even if you pay before the notice.