Handling GST Notices: Jab Supplier Ho Jaye Non-Existent , NGTP or Suspended

Guide on replying to GST notices for suspended or non-existent suppliers. Understand ITC eligibility, DRC-03 voluntary payments, and legal consequences

Rhushikesh C Patil

12/24/20253 min read

Handling GST Notices: Jab Supplier Ho Jaye 'Non-Existent', NGTP or 'Suspended'

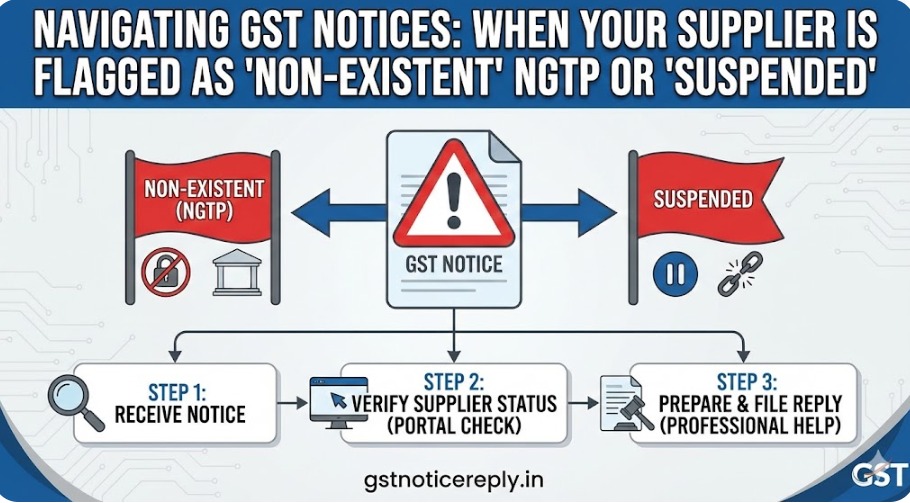

One of the most critical issues currently emerging is the receipt of notices indicating that a supplier has been flagged as 'non-existent NGTP ' or 'suspended'.

This situation is particularly alarming because it directly threatens the validity of your Input Tax Credit (ITC). Failure to address these notices promptly and accurately can lead to substantial tax demands and protected legal battles. This article provides a strategic guide on handling such notices under the CGST Act, 2017.

Understanding 'Non-Existent' or 'Suspended' Suppliers

The GST ecosystem relies on a transparent chain of transactions. When authorities identify a supplier as 'non-existent NGTP ' or 'suspended,' it typically implies:

Fictitious/Bogus Entities: The supplier has no physical place of business and exists only on paper to pass on undue ITC through fake invoicing.

Suspended Registration: The supplier's GSTIN has been suspended or canceled due to fraud, non-filing of returns, or other statutory non-compliances.

Non-Genuine Taxpayer (NGTP): A broad category for taxpayers involved in circular trading or bill-trading without the actual movement of goods or services.

Types of Notices Received

If your supplier is flagged as an NGTP, the department may issue the following:

ASMT-10 (Scrutiny of Returns): Often the initial notice identifying discrepancies between your ITC claims and the supplier's non-compliance.

DRC-01A (Pre-SCN Intimation): An intimation issued before a formal Show Cause Notice, providing an opportunity to pay the tax or provide a clarification.

DRC-01 (Show Cause Notice): A formal demand proposing tax recovery, interest under Section 50, and penalties under Section 73 or 74.

REG-17/18: While directed at the supplier, you may receive inquiries to verify the genuineness of past transactions with that entity.

Strategic Option: Voluntary Payment via DRC-03

If an internal audit reveals that the supplier was indeed non-existent or if you lack sufficient evidence (like E-way bills or proof of delivery) to prove the transaction, accepting the error and paying via Form DRC-03 may be the most viable path.

Benefits of this approach:

Avoids Litigation: Voluntary payment helps close the case without entering a long-drawn legal battle.

Reduction in Penalty: Paying before the issuance of a formal Show Cause Notice (SCN) can lead to a complete waiver or significant reduction in penalties under Section 73 or 74.

Time Efficiency: It allows the business to focus on operations rather than responding to multiple summons and hearings.

Important: This option signifies an admission of liability. Ensure you consult a tax expert to calculate the exact interest and tax components before filing DRC-03.

Consequences of Not Replying to GST Notices

Ignoring a notice regarding a non-existent supplier is highly detrimental. The legal consequences include:

Ex-parte Order: If you fail to submit a reply within the deadline, the proper officer can pass an order based solely on the department's findings, confirming the entire demand.

Blocking of ITC: The ITC claimed against invoices from the flagged supplier will be permanently disallowed, and blocking of ITC requires you to reverse the credit in cash.

Mandatory Interest: Under Section 50, interest will be charged on the wrongly availed ITC from the date of availment until the date of payment.

Heavy Penalties: Penalties can range from 10% to 100% of the tax amount, especially if the department invokes Section 74 (Fraud/Willful Misstatement).

Recovery Proceedings: The department has the power to attach bank accounts and seize assets to recover the confirmed tax dues.

Audit Risk: Failing to reply flags your GSTIN as "High Risk," increasing the likelihood of comprehensive department audits in the future.

Conclusion

When a supplier is flagged as 'Non-existent,' the burden of proof regarding the genuineness of the transaction lies heavily on the buyer. Whether you choose to contest the notice or settle the demand via DRC-03, a timely response is non-negotiable. Proactive compliance is the only way to safeguard your business from the harsh recovery provisions of the GST law.

We’re here to help!

If you need a professional, ready-to-use Reply Draft in Word or PDF format, connect with us on WhatsApp at 9224161099.