Draft Reply Format for Notice of NGTP or Suspended Suppliers

Download our professionally drafted reply format for GST notices regarding Non-Genuine Taxpayers (NGTP) or suspended suppliers. Learn how to respond to ITC blocking under Rule 86A and SCNs for non-existent vendors

Aman K Patel

12/25/20252 min read

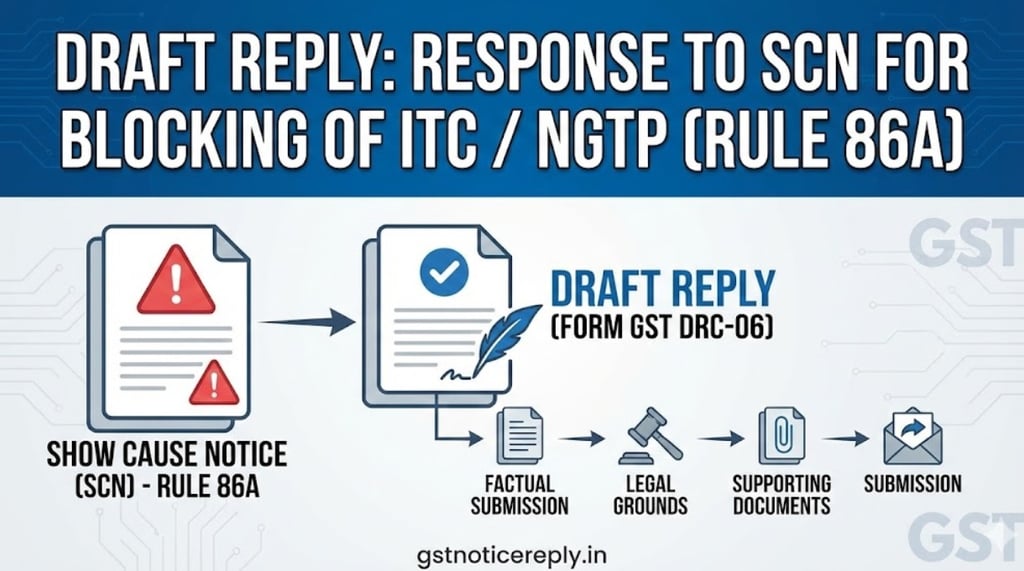

Draft Reply: Response to SCN for Blocking of ITC / NGTP (Rule 86A)

Introduction

Receiving a notice regarding a Non-Genuine Taxpayer (NGTP) or a Suspended Supplier is one of the most complex challenges in the GST regime. In such cases, the department often questions your Input Tax Credit (ITC) on the grounds that the supplier is non-existent or fraudulent. To safeguard your business from heavy penalties and bank attachments, a timely and legally sound response is mandatory.

Common Types of Notices Received

When a supplier is flagged, you may receive the following notices:

ASMT-10: A scrutiny notice pointing out discrepancies in ITC.

DRC-01A: A pre-Show Cause Notice (SCN) intimation providing a chance to pay or clarify.

DRC-01: A formal Show Cause Notice proposing demand, interest, and penalties.

Rule 86A Order: An order from the Commissioner blocking your Electronic Credit Ledger.

Professionally Drafted Reply Format

Below is a standard template for a reply to a Show Cause Notice where the taxpayer chooses to reverse ITC via DRC-03 to avoid further litigation.

To,

The Proper Officer,

GST Department,

[Mention Ward/Circle and City]

Subject: Reply to Show Cause Notice No. [Insert SCN Number] regarding Non-Existent/Suspended Supplier.

Respected Sir/Madam,

With reference to the captioned notice, we, [Your Business Name], GSTIN [Your GSTIN], submit our reply as follows:

Fact of the Case: We are informed via the SCN that our supplier, M/s [Supplier Name], has been flagged as 'non-existent' or 'suspended'.

Due Diligence Performed: We state that at the time of the transaction, we verified the GST portal, and the supplier’s status was 'Active'. We are in possession of valid tax invoices and have received the goods in full compliance with Section 16 of the CGST Act, 2017.

Voluntary Reversal: Without prejudice to our legal rights and without admitting any fraudulent intent or willful misstatement on our part, we wish to state that we are a law-abiding taxpayer. At the time of the transaction, we had exercised due diligence, possessed valid invoices, and made payments through banking channels. However, to maintain a healthy compliance record and to avoid the hardships of a prolonged legal battle and potential interest/penalty burdens, we have decided to voluntarily reverse the disputed ITC.

Payment Details: We have reversed the tax amount of Rs. [Amount] along with applicable interest under Section 50 via Form GST DRC-03 (ARN: [Insert ARN] Dated: [Date]).

Prayer: Since the disputed tax has been paid back to the Government, we most humbly request your good office to drop the proceedings, unblock our ITC (if blocked under Rule 86A), and issue an acknowledgment.

We assure you of our continued cooperation with the Department.

Thanking you,

Yours faithfully,

Conclusion

When a supplier is flagged as Non-existent / NGTP / Suspended, the burden of proof regarding the genuineness of the transaction lies heavily on the buyer. Whether you choose to contest the notice or settle the demand via DRC-03 to avoid a long legal battle, a timely and well-documented response is non-negotiable.

Proactive compliance—such as verifying suppliers periodically and maintaining robust documentation—is the only way to safeguard your business from the harsh recovery provisions of the GST law.

Pro Tips -

Drafting Support: Use the draft reply provided in our previous post to structure your formal response.

Voluntary Payment: If you choose to reverse, ensure you calculate interest at 18% under Section 50

Enclosure: A strong reply should always include the following documents Copy of the Tax Invoices, Bank Statements showing payment to the supplier, a Copy of the filed DRC-03, and a payment receipt.