A Guide to Handle ASMT-10 Notices for GSTR-2B vs. GSTR-3B ITC Mismatch

A Guide to Handle ASMT-10 Notices for GSTR-2B vs. GSTR-3B ITC Mismatch

Rhushikesh C Patil

12/20/20253 min read

GST Portal pe login kiya aur ASMT-10 dikh gaya? Seeing a notice in the 'View Additional Notices' tab can feel like an uninvited guest at a party. It’s that moment of "Ab kya karein?"

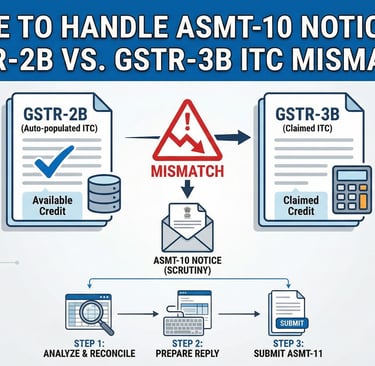

If your Input Tax Credit (ITC) claims as per GSTR3B don't match your supplier's filings, you are likely to receive a notice in Form GST ASMT-10. This is a scrutiny notice issued under Section 61 of the CGST Act 2017. But don't panic—an ASMT-10 is not a fine; it is an opportunity to clarify.

What is Section 61? The "Scrutiny of Returns"

Section 61 empowers the GST department to verify the correctness of the returns you have filed. Think of it as a preliminary, automated, or semi-automated check to ensure "Sab sahi hai na?"

The "Proper Officer" (your jurisdictional Superintendent or Assistant Commissioner) reviews your returns (GSTR-1, 3B, 9) against data available in GSTR-2A/2B. Under Rule 99 of the CGST Rules, if they spot a discrepancy, they are legally required to inform you and seek an explanation before taking any harsh recovery action.

The Main Culprit: GSTR-2A/2B vs. GSTR-3B Mismatch

While there are several reasons for a notice, the most frequent reason for receiving an ASMT-10 today is the ITC Mismatch.

The Discrepancy: You claimed ₹100 as ITC in your GSTR-3B, but your suppliers only reported ₹95 in their GSTR-1.

Why does it happen:

Suppliers forgot to file their GSTR-1.

Suppliers filed GSTR-1 late (Timing difference).

Incorrect GSTIN entry (B2B vs B2C error).

ITC on Import of Goods (Sync issues with ICEGATE).

Pro Tip: For older periods (FY 2017-18 and 2018-19), refer to Circular No. 183/15/2022, which allows taxpayers to rectify these mismatches using CA certificates or self-declarations. For FY 2019-20 and 2020-21, see Circular No. 193/05/2023 for similar relief.

How to Respond: The ASMT-11 Process

Understanding the Notice (ASMT-10)

When an officer finds a mismatch, they issue Form GST ASMT-10 electronically on the portal.

What it contains: It lists the specific tax period, the nature of the discrepancy (e.g., "Excess ITC availed" or "Short payment of tax"), and the quantified tax, interest, or penalty amount.

Time Limit to Reply: You generally have 30 days (or the period specified in the notice) to file your explanation.

How to Reply (Form ASMT-11)

Your response must be filed electronically through the GST portal in Form GST ASMT-11. You have two choices:

Option A: Accept the Discrepancy

If the error is genuine (e.g., you accidentally claimed double ITC), you should:

Pay the tax + interest via Form DRC-03.

Mention the ARN of the DRC-03 in your ASMT-11 reply.

Option B: Explain/Contest

If the mismatch is due to a timing difference or supplier error, do not just give a narrative reply. Provide a clear table. You must provide:

A detailed Reconciliation Statement.

Copies of tax invoices.

Proof of payment to suppliers.

Communication with suppliers asking them to rectify their GSTR-1.

File ASMT-11 on the Portal

Go to Services > User Services > View Additional Notices.

Click 'Reply' and upload your explanation and supporting documents (Invoices, Ledger, CA Certificates).

Payment (if required): If you find an actual error, pay the tax + interest (u/s 50) via Form DRC-03 and attach it to your reply.

The End Result: ASMT-12 or SCN?

Success: If the officer is satisfied, they will issue Form GST ASMT-12, dropping the proceedings. "Case Closed."

Risk: If you don't reply or the reply is unsatisfactory, the officer can escalate this to a Show Cause Notice (SCN) under Section 73 (Normal) or Section 74 (Fraud/Willful Misstatement).

Conclusion

An ASMT-10 notice for ITC mismatch is not an order to pay; it is a request for a "Safai" (explanation). By using a data-driven approach and citing the relevant circulars, most of these notices can be closed at the scrutiny stage itself.

Also, it is crucial to know if the notice you received is "time-barred." While Section 61 itself doesn't list a specific expiration date for issuing ASMT-10, it is governed by the overall limitation periods for issuing demand orders under Sections 73 and 74.

Click here to read our Complete guide for 2025 - Time limit for issuing GST Notice https://gstnoticereply.in/time-limit-for-issuing-gst-notice-under-section-73-and-74-a-complete-guide-for-2025

We’re here to help!

If you need a professional, ready-to-use ASMT-11 Reply Draft in Word or PDF format, connect with us on WhatsApp.